Don't Wait: Open Enrollment Is the Time to Reevaluate Your Needs

With premiums rising, out-of-pocket limits climbing, and new rules on the horizon, this year’s Open Enrollment isn’t just routine—it’s a turning point. Here’s what employers need to know (and do) to stay ahead.

In This Article

Open Enrollment is coming fast

Open Enrollment is a designated period of time each year in which employers and employees can review their current benefits and make changes to insurance coverage, add or remove dependents, or change plans completely. For 2026 coverage, the Open Enrollment period starts on November 1st. That’s only a few days away, so HR teams and business owners should already be preparing for it! And because the window is short, your employees should be familiarizing themselves with their current benefits, changes to their plans, and any new options that they might benefit from. That way, when Open Enrollment actually starts, they can take full advantage of your benefits package!

Open Enrollment timeline

- October 15, 2025 – Medicare Annual Enrollment Begins

- November 1, 2025 – Marketplace (ACA Individual & Family Plans) Open Enrollment Begins

- December 7, 2025 – Medicare Annual Enrollment Ends

- January 15, 2025 – Marketplace (ACA Individual & Family Plans) Open Enrollment Ends

What’s new in 2026

Each Open Enrollment season brings with it some new dynamics and challenges, and 2026 is no exception. This year, small business employers and HR teams will be dealing with rising health insurance premiums, higher out-of-pocket limits, and policy changes that will soon shorten the Open Enrollment window itself. For many, the effect these types of changes have on employees’ budgets are front of mind, so let’s take a look at how your employees might be impacted.

Premiums Are Going Up

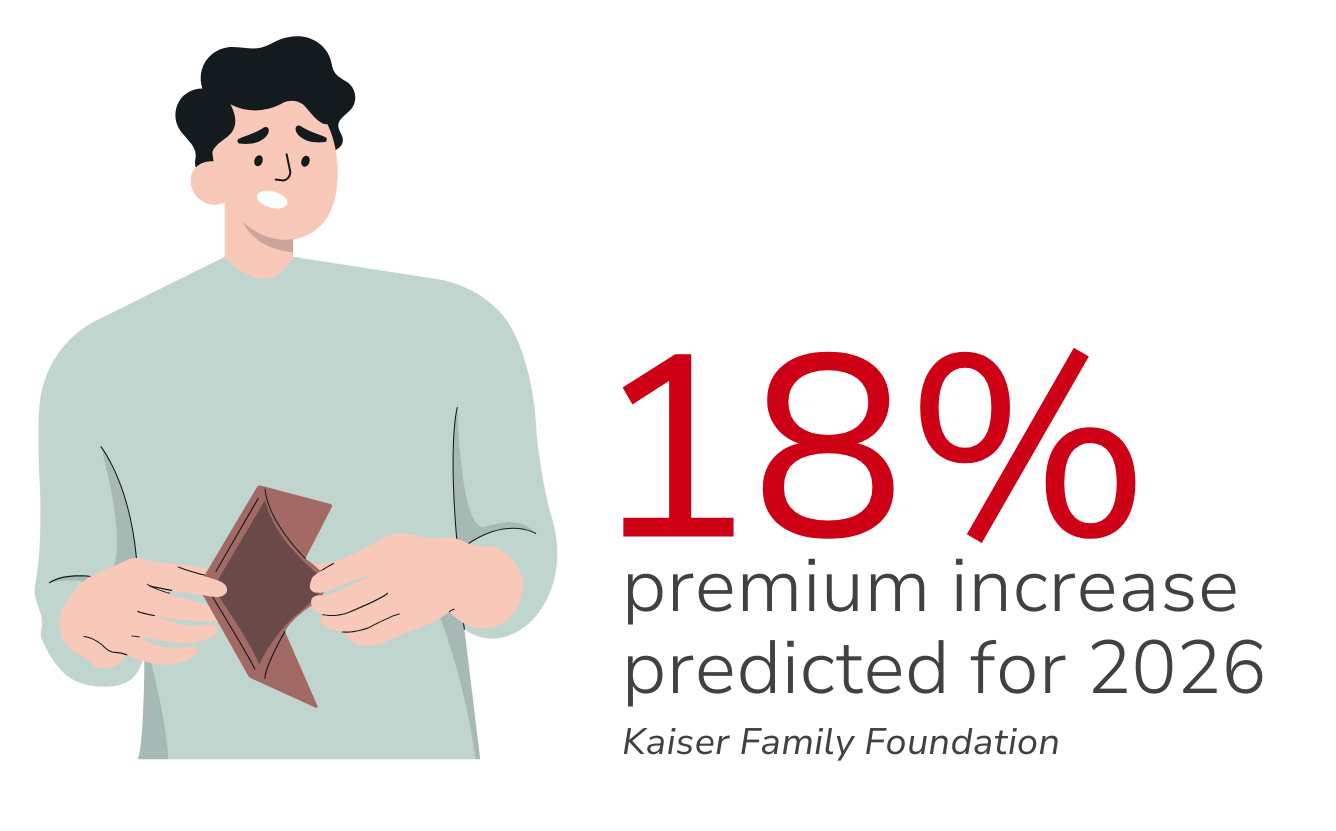

Health insurance costs are set to climb in 2026, and employers and employees will both feel it. According to a Kaiser Family Foundation report, ACA Marketplace insurance carriers are forecasting a median premium increase of 18%, which will be the highest single-year jump since 2018. As the employer, this could have a bigger effect on your operation than you realize.

Out-of-Pocket Maximums Are Going Up

Premiums aren’t the only expense that’s climbing. The out-of-pocket maximum, the most an individual or family must spend before their plan covers 100% of the costs, has been on the rise for years. For single coverage under ACA-compliant plans, this maximum has increased from $6,350 in 2014 to $9,100 in 2023, a 43% increase. For 2025, this maximum has risen to $9,200, and projections for 2026 suggest it could reach $10,600 for individuals and more than $21,000 for families.

For employers, rising out-of-pocket limits mean that even though your company may help cover premiums, employees may still face steep costs in seeking healthcare. This can lead to delayed treatments, financial strain, lower satisfaction with your benefits, and less desirable health outcomes.

Shortening Open Enrollment Window

One development that is less urgent but should warrant your attention, nonetheless, is the upcoming shortening of the Open Enrollment window, beginning with coverage for 2027. This means that the shortened Open Enrollment period won’t take effect until Open Enrollment time toward the end of 2026. This Open Enrollment cycle will stay the same, but employers should be paying attention because their employees next year will have less time to do research, review their plan options, and make decisions.

Forward-thinking employers should start thinking about and planning now how they will help prepare their employees ahead of time.

The costs of inaction

When businesses stick with the same benefit plans year after year without reevaluating, they certainly avoid short-term hassle, but they and their employees will pay for it in the long term. Given how fast premiums, deductibles, and out-of-pocket maximums are rising, inaction isn’t likely to provide a net-neutral result. It will likely mean overpaying and missed savings for both you and your employees. For small-and medium-sized businesses, choosing to not explore alternatives or negotiate better plans can eat into your margins and eventually wear away employee goodwill.

According to a report by Becker’s and JP Morgan, businesses with fewer than 50 employees saw premiums rise by 33% from 2018-2023, while total payroll increased by 42% over the same period. This should tell us just how much health insurance is becoming a larger portion of business costs, particularly for smaller companies.

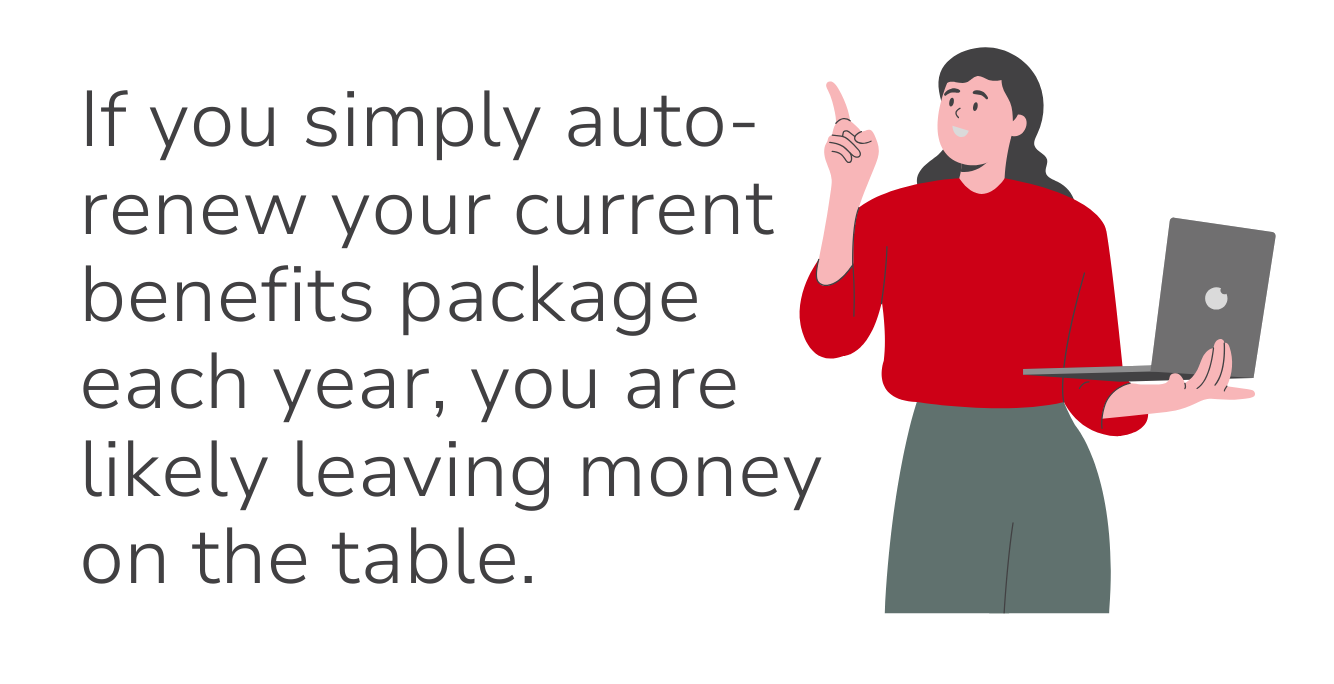

That means that if you simply auto-renew your current benefits package each year, you are likely leaving money on the table. Taking the time to research and weigh your options usually translates into healthy savings for your business.

Questions to ask before renewing your plan

Here are three questions every business owner or decision maker should ask before reviewing benefits:

1. Are there alternative products that could lower costs while keeping similar benefits? Don’t assume last year’s carrier or plan tier is still the best value for you. Request quotes and compare designs!

2. What is the total cost of coverage, including premiums and employee out-of-pocket exposure? Lower premiums often shift more burden to the employees in the form of deductibles, coinsurance, or limits/caps. Understanding the total exposure can help avoid surprises for you and your employees.

3. When was the last time you benchmarked your benefits against similar competing businesses in your area/industry? Market rates, regulations, and provider networks can shift. What was competitive five years ago may be overpriced today!

Exploring alternatives

As traditional insurance costs keep going up and Open Enrollment windows start to tighten, small businesses can benefit from more flexible and cost-effective benefit options. Gone are the days where nontraditional alternatives are just backup plans. They have now become viable primary benefits that often align better with both employer and employee budgets. Planstin helps businesses explore these options, combining both traditional insurance with nontraditional alternatives to create solutions that don’t sacrifice affordability for value, or vise-versa.

Small businesses just getting their foot into the benefits door might consider:

Direct Primary Care (DPC) Membership

Where members pay a flat fee to have access to a primary care provider. This alternative arrangement helps bypass copays and restrictions found in traditional insurance networks.

HealthShare Membership

Where members contribute to a community fund that is used to assist with eligible healthcare expenses. These tend to have lower monthly costs than traditional health insurance and aren’t bound to Open Enrollment windows.

Virtual Care Membership

Where subscribers similarly pay flat fees to have virtual (either over the phone or online) access to healthcare providers. This is increasingly becoming an affordable way to manage routine healthcare needs while avoiding high premiums and out-of-pocket costs.

It’s worth noting that in another big upcoming change, starting in 2026 HSA funds can now be used to pay for certain nontraditional healthcare services, like DPC and Telemedicine. You can read more about this development here.

Next steps with Planstin

Planstin is here to help businesses like yours handle daunting changes like increasing costs and tighter deadlines. Our expert team works to build benefits packages that play to the unique strengths and needs of companies of all sizes. You get traditional coverage where it counts, and innovative alternatives, like direct primary care, where they make the most sense.

And this doesn’t just save money. It makes you a more appealing employer, helping you recruit and retain employees. According to a recent survey, 82% of workers say health benefits are a top factor in deciding whether to accept a job offer.

Letting your benefits stagnate doesn’t just risk higher premiums. It can drive up turnover, cost you talent, and hurt your employee morale and productivity.

Reach out to Planstin today to schedule a benefits review before Open Enrollment. Together, we can make sure your employees have access to the most cost-effective solutions that fit your budget and their needs.

Have questions about Open Enrollment or looking to explore alternatives? Let’s talk.

Explore

SUGGESTED FOR YOU