Benefits Trends for 2026

Benefits are getting more expensive, and traditional models are cracking under the pressure. In 2026, businesses will need smarter, more flexible ways to care for their teams.

In This Article

The outlook for employee benefits in 2026 doesn’t look overly optimistic. Health insurance costs are going up, as are employee expectations, and employers are left in the middle trying to juggle budgets and values. But finding solutions in the coming year may take some creativity in how businesses choose to design and deliver benefits to their workers. Traditional insurance models may not work for small- and medium-sized businesses facing tough decisions.

In this article, we’ll take a look at the top trends affecting benefits in 2026. Some are related to costs of insurance, and others are tied to employee needs for flexible or optional programs. We at Planstin see the future in alternative solutions and innovations in plan design, so we’ll also be spotlighting one of our newest plans that’s just entered the market: Care+ Direct, a non-insurance approach that makes care more affordable and accessible for your employees.

Trend #1: Health insurance premiums are increasing

There doesn’t seem to be any way around it: premiums are going up.

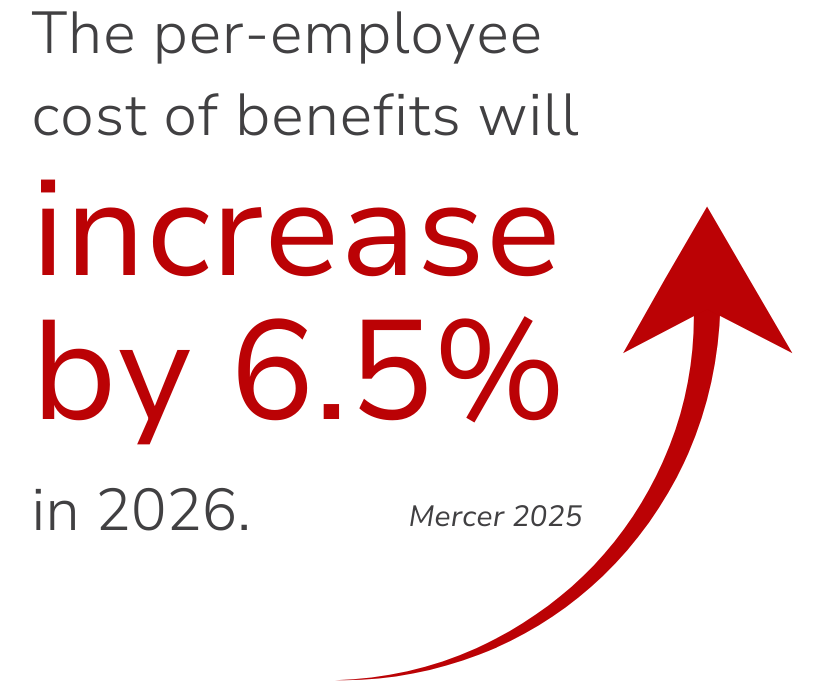

According to a 2025 Mercer survey, employers are expecting their per-employee cost of benefits to increase by an average of 6.5% in 2026, while recent KFF data shows that premiums for family coverage have almost reached $27,000 per year.

If you’re running a small- or medium-sized business, ask yourself this: Are you expecting your budget to increase by 6.5% in 2026? Many are not, and it’s a real concern. Without comparable budget growth, these businesses are going to feel pressure to reduce benefits or shift more costs to the employee.

Trend #2: Employers are shifting more costs to employees

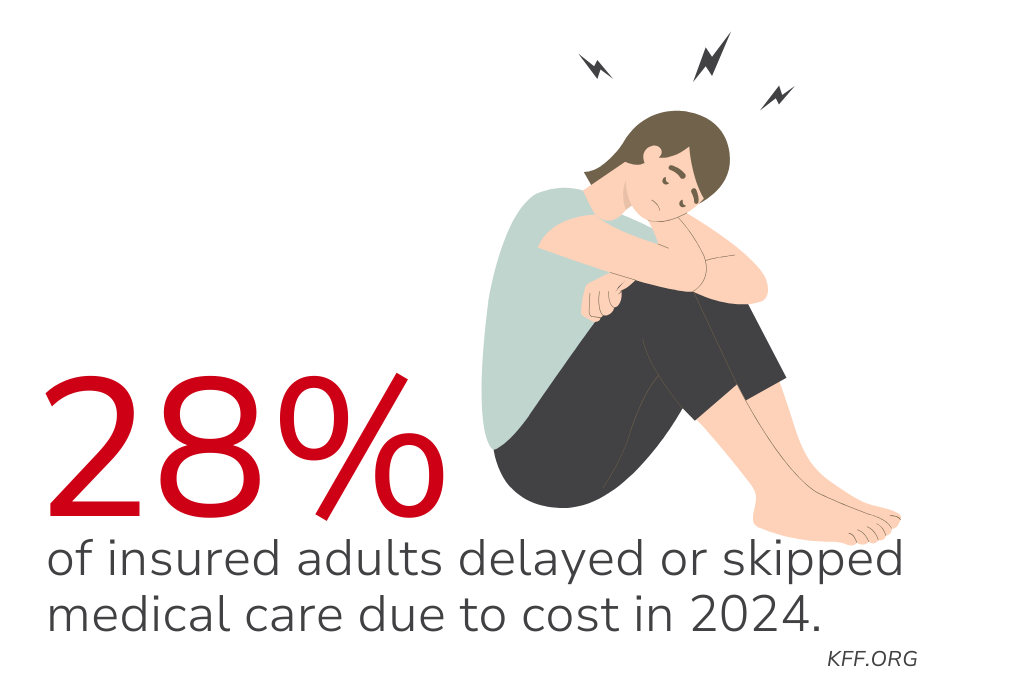

With costs going up, employers are preparing to pass more of the costs to their workers. In 2026, employees can expect their deductibles, copays, and coinsurance costs to all go up as their employers manage the increased expenses. Some smaller companies have already cut back their offerings to only high-deductible health plans, per KFF. And while these types of plans do keep premiums lower, they don’t always make healthcare easier to access. In fact, KFF has found that 28% of insured adults delayed or skipped medical care due to cost in the past year.

So, while the coverage may be there, the worker’s situation or access isn’t necessarily relieved by it.

Trend #3: A focus on access to primary care

One of the more visible shifts already in effect and expected to continue into 2026 is the push to improve how quickly and easily workers can get primary care. Employers are already in the know: better access to primary care leads to earlier intervention, lower costs, and better health outcomes. A report by the Primary Care Collaborative found that organizations investing in primary care models see reductions in emergency visits and improved management of chronic conditions.

To make this possible, many companies are redesigning their health plans to guarantee faster and easier access through new and innovative solutions. Direct Primary Care (DPC) memberships and Virtual DPC options are increasingly being included in benefit offerings, giving employees access to relationship-based care without the traditional barriers of waiting rooms or ever-increasing copays.

Trend #4: A focus on mental wellness and voluntary benefits

Another trend that has been building for some time and doesn’t look to slow down in 2026 is the growing support for mental health in benefits offerings. SHRM’s 2024 employee benefits survey found that the number of employers offering some form of mental health program has grown immensely since the pandemic years, with over 90% of employers now offering such benefits.

In tandem with this, other voluntary benefits are also becoming an increasingly important part of benefits packages. These are the add-on style options that allow employees

to customize their coverage to their circumstances, including supplemental health coverage, financial wellness tools, or other lifestyle-focused programs. These types of opt-in benefits are proving a practical solution for small- and medium-sized businesses trying to add real value without multiplying costs for themselves.

Trend #5: More employers are using alternative plans and models

Traditional health insurance plans are becoming more expensive each year, and as discussed above, employers and employees are starting to opt out entirely. But, they aren’t all simply choosing to go without! There are alternative solutions out there that are starting to gain traction.

One such solution is level-funded plans. KFF’s 2025 survey reports that 51% of insured workers in companies with 10-199 workers are enrolled in a level-funded plan, up from 19% in 2018.

Employers are also increasingly offering benefits like telemedicine, standalone prescription programs, and other cost-saving tools that give employees better care without significant effects to premiums.

The future in alternatives and innovations

One thing seems clear from this list: both employers and employees want options that aren’t subject to constantly rising premiums and constrained access to the care they’re paying for. That’s why alternative options are starting to get more attention. And it’s why Planstin is constantly refining and innovating its non-traditional packages, like our new Care+ Direct plan.

Care+ Direct gives your employees more care with fewer costs. By using an included primary care membership and coordinated care pathway, your employees can get access to care and have their typical out-of-pocket costs waived. That means no deductibles, no copays, no coinsurance. In short, no surprises.

Are your benefits keeping up? Let’s talk.

Explore

SUGGESTED FOR YOU