Renewal Isn't a Strategy: Why Reactive Benefits Design Keeps Employers Stuck

When renewal season arrives, most benefit decisions get made under pressure and on a short timeline. That pattern has a cost.

In This Article

When renewal season arrives, it tends to compress everything. Carriers present updated rates. Advisors pull together options. Employers weigh the increases, make adjustments, and move on. It is a familiar process, and for most organizations it has been repeated enough times that it starts to feel like a system. But familiarity is not the same as strategy.

The problem is not that benefits get reviewed at renewal. The problem is that the conversation tends to narrow quickly to rate comparisons, and the underlying structure of the plan rarely comes up for serious examination. Decisions made under deadline pressure tend to preserve the existing structure rather than question it. Over time, that pattern produces benefit plans that were never really designed so much as inherited and incrementally adjusted.

Reacting to rates is not the same as managing costs

Rate comparisons measure carrier pricing. They do not measure whether the underlying benefits design is aligned with how the workforce actually uses care, whether the funding mechanism makes sense for the employer’s situation, or whether the plan is generating the kind of pricing discipline that leads to long-term cost stability.

An employer can accept the lowest available rate every year for a decade and still see sustained cost growth, because the rate reflects the underlying plan. If the plan is structurally reactive, its cost trajectory will be too. Aon’s 2025 Health Survey projects that U.S. employer health care costs will rise an average of 9.5% in 2026, the highest projected increase in over a decade, even after accounting for planned cost-reduction measures. Accepting the lowest renewal rate each year has not bent the curve.

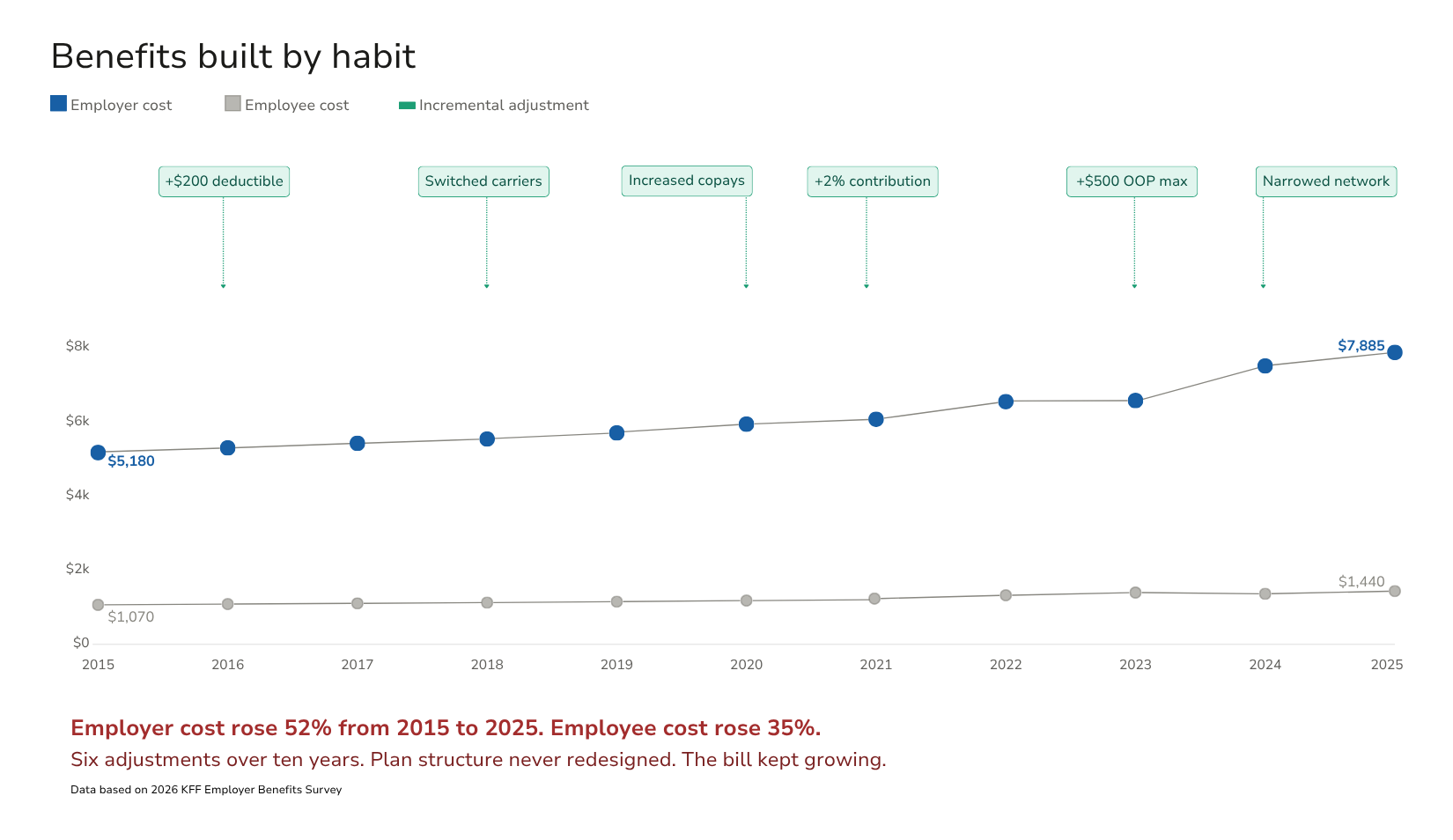

Benefits built by habit

When benefits reviews focus primarily on rates, structural assumptions rarely get examined. Copay levels, deductible structures, funding mechanisms, and network configurations tend to persist not because they have been evaluated and found to be optimal, but because changing them requires deliberate effort that the renewal window does not naturally create space for.

Choosing between carriers is a procurement decision. Designing a benefits strategy is a different exercise entirely.

The result is benefit plans built by habit. They reflect decisions made years or even decades ago, layered with incremental adjustments that responded to cost pressure without addressing its source. Employers often cannot fully articulate why their plan is structured the way it is. The answer, if traced back far enough, is usually some version of “because that’s what we had last year.”

The most common reactive adjustment is shifting more cost to employees through higher deductibles or increased premium contributions. But it has a limit. The

KFF 2025 Employer Health Benefits Survey found that more than a third of covered workers are already enrolled in a plan with a deductible of $2,000 or more for single coverage, and nearly half of large employers report that their employees have “high” or “moderate” concern about current cost-sharing levels. Cost shifting is not a strategy. It is a pressure valve, and for many employers it is running out of room.

What it looks like to design before you default

The employers beginning to think differently are not abandoning the tools that work. For many, a traditional PPO network still serves a legitimate purpose. The goal is not to replace every existing structure, but to make deliberate choices about it rather than inheriting it. That starts with questions the renewal process rarely creates space for: What is actually driving claims cost in this workforce? Is the current funding structure the right fit? Are there care delivery options such as direct primary care, reference-based pricing, or centers of excellence that could improve outcomes while reducing cost?

These approaches require deliberate design decisions that cannot be made under renewal-window pressure, because they involve changing the plan’s architecture, not just its carrier. They are also not reserved for the largest employers. They are increasingly accessible to mid-size and smaller organizations that have both the flexibility and the urgency to explore them. What they typically require is an advisor who arrived before the renewal quote, with a different kind of conversation already underway.

Employers who approach benefits this way, and advisors who help them do it, are treating benefits as a strategic function rather than a reactive administrative task. That shift changes what options are visible, what decisions are possible, and what outcomes are achievable over time.

The bottom line

Benefits built by habit tend to produce costs that rise by habit. The employers who break that pattern are the ones who started a different conversation before the renewal window opened, and the advisors who led that conversation are the ones who will matter most in the years ahead.

Strategy starts before the quote. Before the network comparison. Before the carrier menu. The advisors who lead the next era of benefits won’t just manage renewals. They will design strategy.

Ready to stop fighting an outdated system and start building benefits that work?

Explore

SUGGESTED FOR YOU