The Myth of PPO Savings

When discounts are calculated from inflated list prices, they can create the illusion of savings without addressing the underlying cost of care. Understanding how these pricing mechanics work is an important first step for employers trying to manage healthcare spending more effectively.

In This Article

Why discounts aren’t always the same as savings

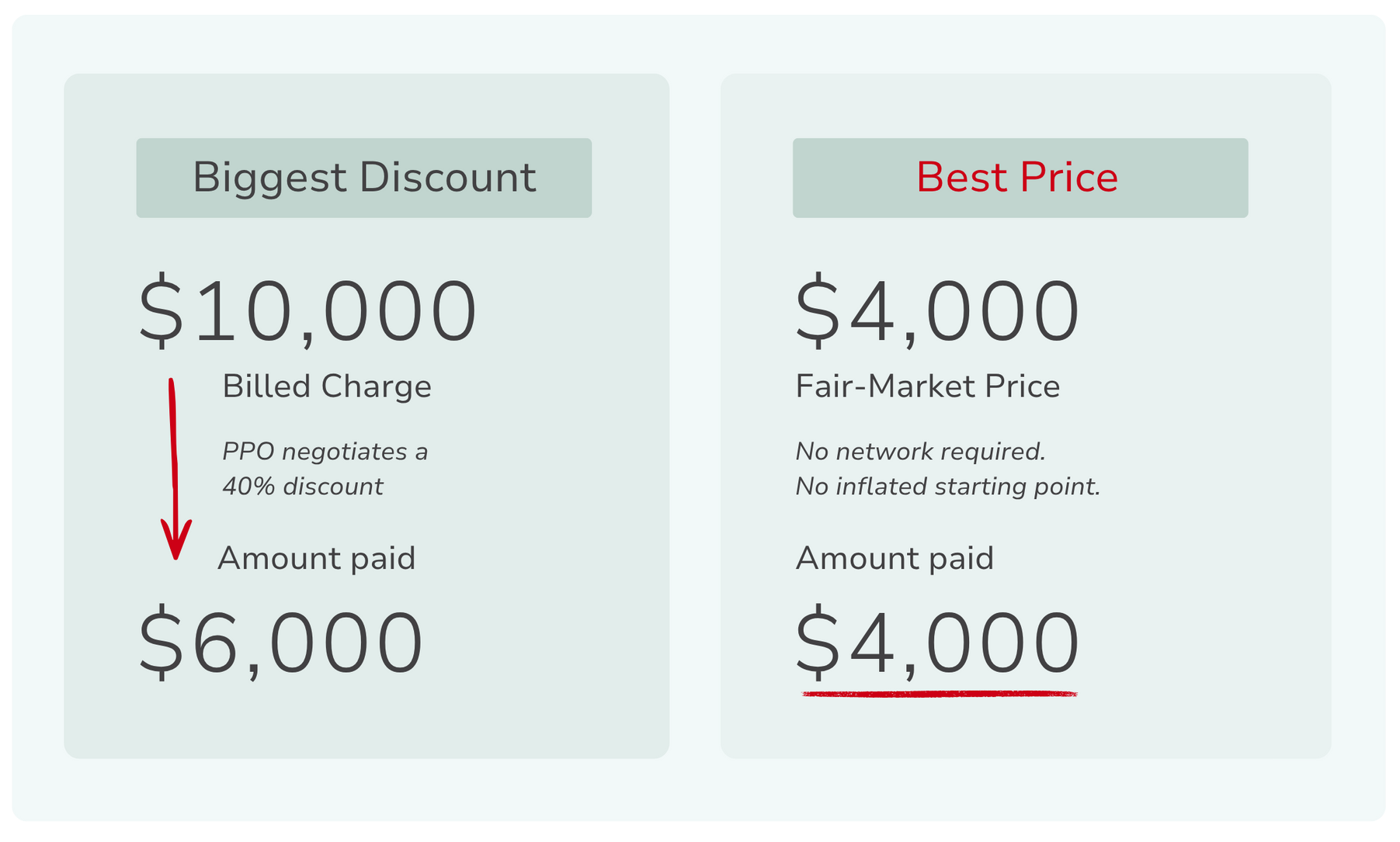

For decades, PPO networks have been positioned as the cornerstone of employer health plans. Advisors, carriers, and plan reports often highlight negotiated discounts as evidence that the system is working. A hospital may bill $10,000 for a procedure, a PPO contract reduces the allowed amount to $6,000, and the plan reports a 40% savings.

On paper, that sounds like a powerful cost-control mechanism, and employers understandably assume the network is successfully negotiating lower prices on their behalf. But if those discounts truly produced meaningful savings, employers would expect healthcare costs to stabilize—or at least grow more slowly. Instead, premiums have continued to rise year after year. That disconnect raises an important question: If PPO discounts are so effective, why do costs keep climbing?

The answer lies in how those discounts are calculated and in the starting prices they’re measured against.

The discount percentage alone tells us very little about the price that ultimately matters: the actual price of the care.

The starting price was never real

Hospitals maintain a comprehensive internal price list for services known as a chargemaster. These lists assign a price to every procedure, test, supply, and service a hospital provides. Research from KFF notes that these list prices can differ dramatically from the amounts insurers and patients ultimately pay. Rather than reflecting the actual cost of providing care, chargemaster prices function primarily as an anchor for negotiations between hospitals and insurers.

Because PPO discounts are calculated from these list prices, the starting number significantly shapes the size of the reported discount. If the list price is high enough, even a steep discount can still leave the final price well above what the service might cost in a more transparent market. This is why the percentage itself can be misleading.

In other words, a large discount does not necessarily mean a fair price.

Why discount percentages can be misleading

In most industries, discounts reduce a price that is reasonably close to the market value of a product or service. Healthcare pricing works differently. When hospitals establish list prices primarily to anchor negotiations, the resulting discounts can appear substantial even when the final negotiated rate remains high.

For employers reviewing plan reports, this creates a distorted signal of value. A report may highlight a 50% or 60% negotiated discount, suggesting the network is delivering meaningful savings. But the percentage alone tells us very little about the price that ultimately matters: the actual price of the care.

Consider two scenarios. A hospital bills $10,000 for a service and the PPO rate reduces it to $6,000 (a 40% discount). Another provider prices the same service transparently at $4,000 with no discount. The first scenario produces a larger reported discount, while the second produces the lower cost. But, most importantly, from the employer’s perspective, only one of those outcomes represents genuine savings.

What independent research shows

Research into hospital pricing has revealed just how wide the gap between list prices and negotiated rates can be.

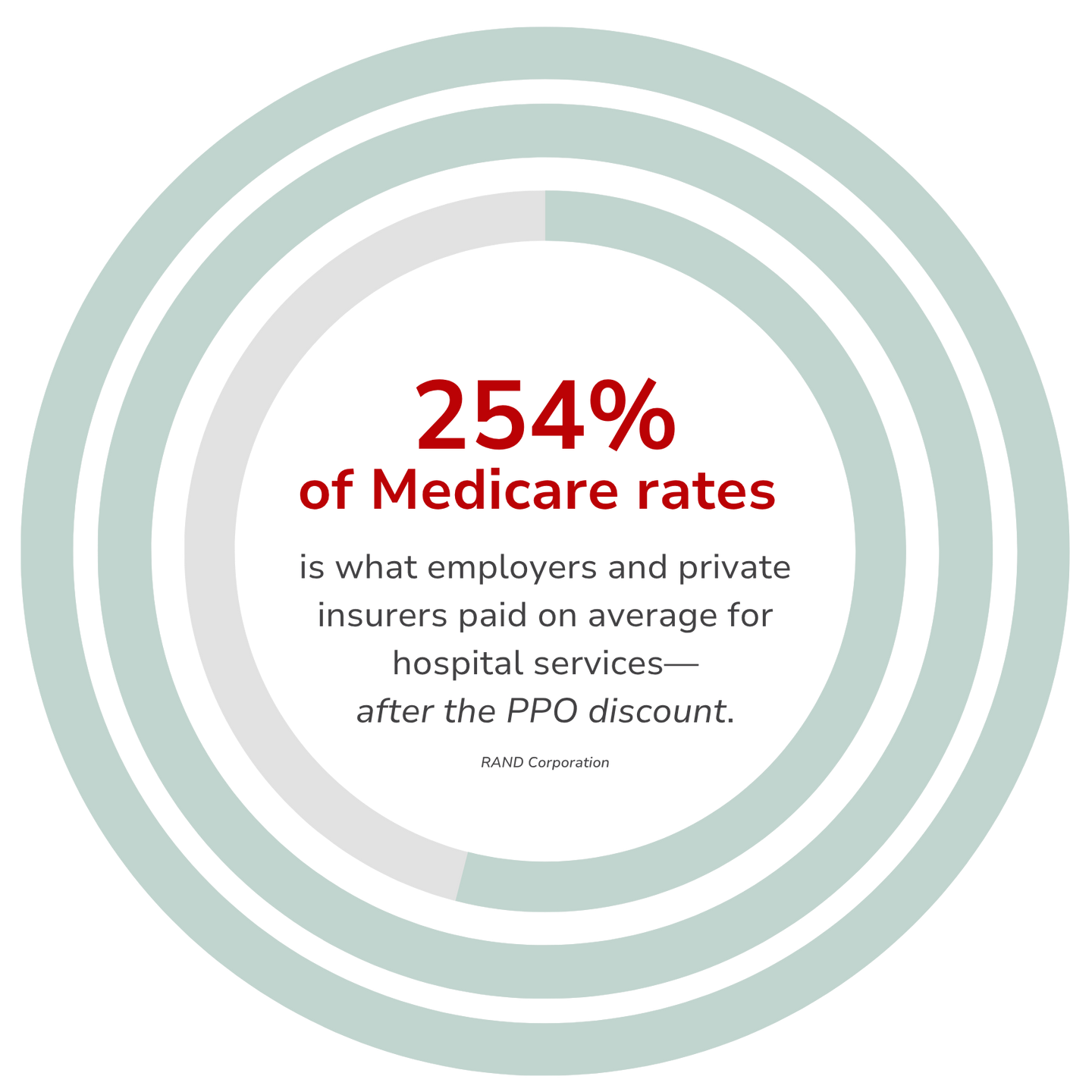

A national study conducted by the

RAND Corporation found that employers and private insurers paid an average of 254% of Medicare rates for hospital services across the United States. The RAND researchers also found that prices for the same services can vary dramatically across hospitals and regions, even within the same insurance networks.

These findings illustrate a straightforward point: a large discount does not guarantee the lowest price. Without visibility into the underlying pricing structure, the percentage alone can create a false sense of cost control.

A better question for employers

For years, employers evaluating health plans have been guided by one primary question: “How large is the network discount?” But focusing on discount size can distract from the metric that matters most.

A more useful question is: “What is the actual price being paid for care?” When employers shift their focus from discounts to real prices, the conversation about healthcare strategy begins to change. Advisors and plan sponsors begin evaluating whether the plan is truly delivering value—or simply reporting large discounts measured against inflated starting prices.

The bottom line

PPO networks were designed to expand access to providers and negotiate pricing agreements with hospitals and physicians. In many cases, they still serve that role. But the industry’s long-standing emphasis on discount percentages can obscure what employers ultimately care about most: the real price of care.

When employers look beyond the reported discounts and examine the mechanics behind pricing, they often discover that those savings are measured against inflated starting numbers. And that realization changes the conversation. Instead of asking: “How big is the discount?” Employers begin asking a more important question: “What should the price have been to begin with?” That question challenges the math behind PPO savings. It also opens the door to a broader conversation about how healthcare benefits are designed and, more importantly, how they might be designed differently.

Ready to stop fighting an outdated system and start building benefits that work?

Explore

SUGGESTED FOR YOU